For company leaders, detailed hiring and workforce data acts as an early warning system for business performance, giving a forward‑looking view that supports better decisions on investment, cost control and competitiveness. By tracking which roles, skills and regions companies are hiring into, leaders can see where competitors are moving into new products, channels and markets – and pinpoint gaps or overexposure in their own strategies.

The effective positioning window on these hiring signals is typically one to three months; by the time market consensus reacts, the underlying data has already shifted. GlobalData Jobs Analytics captures point‑in‑time job postings directly from company career pages, tagged by company, sector and theme. For leaders, this provides a clear view of where investment and capability‑building are still advancing, which markets are slowing, and where demand is starting to build.

This article shows how to look past the headline contraction to identify who is positioning for long‑term nuclear growth – and who is quietly stepping back.

Is nuclear energy hiring slowing?

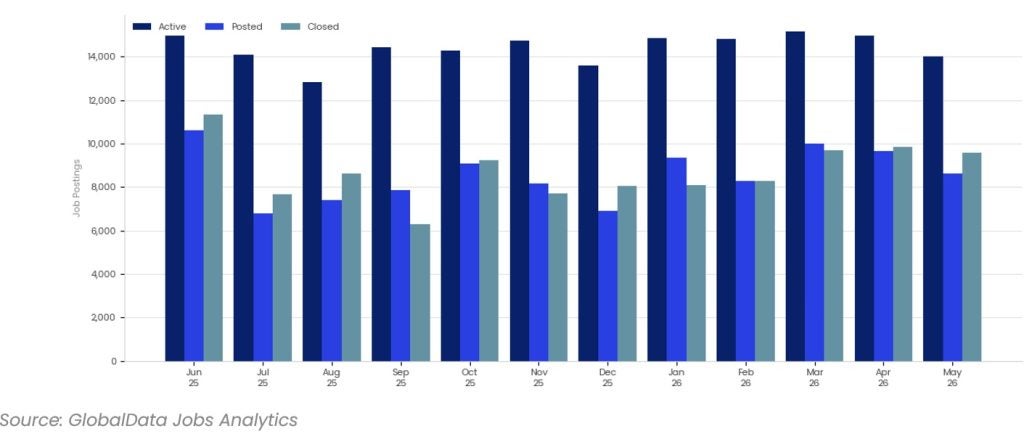

Nuclear energy hiring in North America actually expanded through the second half of 2025, with YoY active posting growth running at 30% to 73% between June and November. However, that cycle has now turned. YoY comparisons have been negative since February 2026, and the latest May 2026 data confirms the sector is in a volume correction. Although the aggregate number conceals a cross-sectional range that is analytically more consequential than the headline. Pure-play nuclear operators are hiring harder into the contraction; services and engineering contractors are pulling back.

Active nuclear postings peaked at 15,167 in March 2026, up from 12,847 at the August 2025 trough. By May 2026, active postings have retraced to 14,016, down 12% YoY. Posted jobs stand at 8,624 for May, down 13% YoY. The inflection is unambiguous: eight consecutive months of positive YoY growth from June 2025 through January 2026, followed by four consecutive months of contraction. June 2025 recorded posted volume of 10,605, the highest in the trailing twelve months, a level May 2026 has not yet recovered.

Closed postings are as informative as active levels. They ran consistently above posted volumes from February through May 2026, signalling genuine drawdown of open role inventory rather than a slowdown in new requisitions alone. The sector is posting less, and filling what it has, faster.

The pure-play nuclear build is running counter to the sector mean

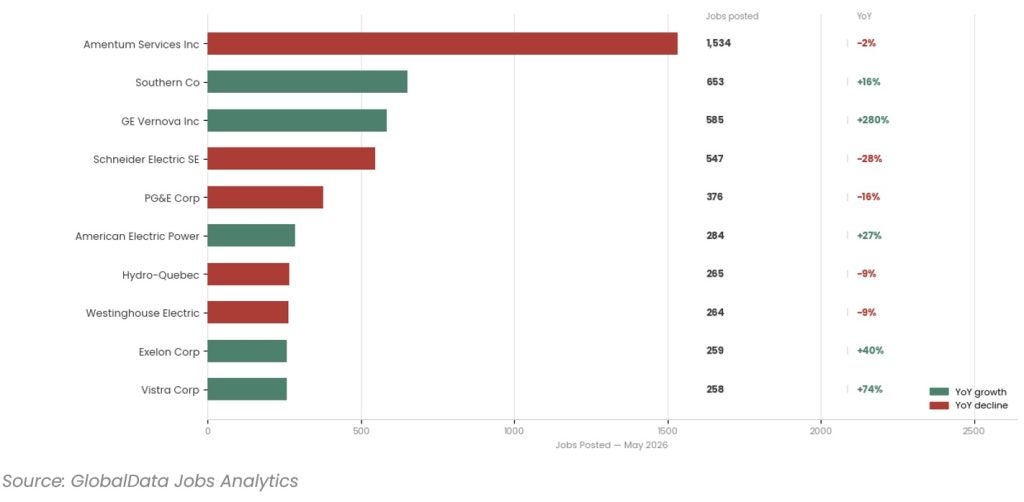

The aggregate contraction masks a split that maps cleanly onto operator type. GE Vernova, the dedicated nuclear equipment and services company spun off from GE in 2024, posted 585 roles in May 2026 against 154 in May 2025, a 280% YoY increase. Vistra Corp, the largest competitive power generator in the US with significant nuclear capacity, is up 74% YoY. Exelon, the pure-play nuclear and regulated utility operator, is up 40%. These are not marginal moves. They are companies with material nuclear exposure choosing to build workforce capacity against a sector-wide contraction.

Against that backdrop, the volume leader Amentum Services at 1,534 postings is down 2% YoY. Schneider Electric, a broad energy management business with nuclear exposure, is down 28%. PG&E and Westinghouse are both down in the mid-teens. The cross-sectional spread between GE Vernova at +280% and Schneider at -28% exceeds 300 percentage points. A portfolio screen built on aggregate nuclear hiring misses all of the directional signal.

Operational scaling, not capability investment

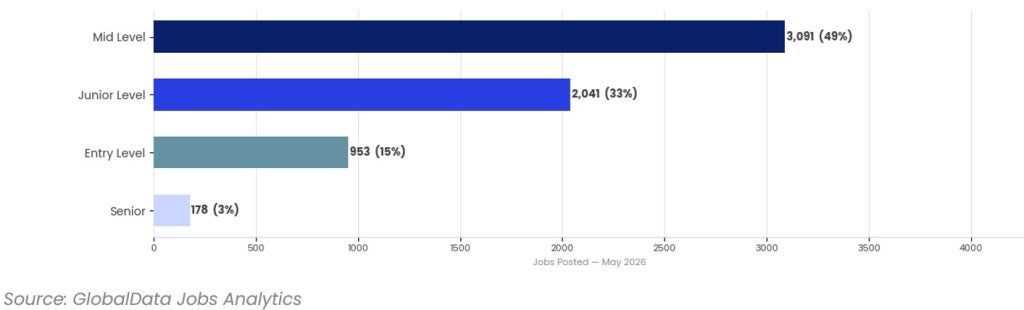

The seniority profile of May 2026 nuclear postings is entry and mid-band dominated to a degree that reads differently from most capital-intensive sectors. Mid-level roles account for 49% of postings, junior for 33%, entry level for 15%, and senior for just 3%. This is the inverse of LNG hiring in the same month, where operators skewed 80% toward mid and senior bands. In nuclear, 97% of postings sit below senior level.

The interpretation is sector-specific. Nuclear operations require large workforces of licensed operators, maintenance technicians, radiation protection specialists and quality assurance personnel at mid and junior levels. The seniority mix reflects the operational headcount requirements of running a fleet, not a preference for depth over breadth. Against that backdrop, what is meaningful is which companies are building senior and specialist hiring into programmes that are otherwise mid-level dominated. Those operators are making a capability statement the aggregate seniority data does not surface.

The thematic composition reflects a sector under regulatory and operational pressure

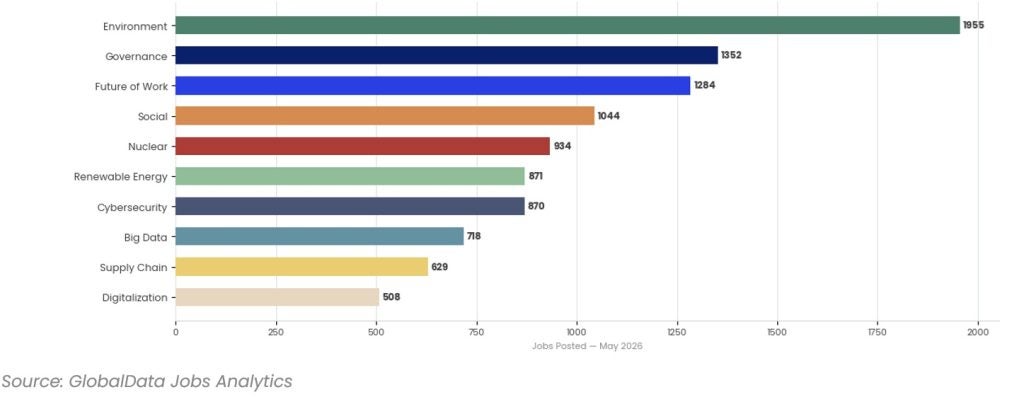

Environment leads all nuclear hiring themes at 1,955 postings, consistent with the compliance and safety reporting obligations that dominate nuclear operational hiring. Governance follows at 1,352, reinforcing the regulatory burden signal. Together they account for the two largest thematic categories, ahead of Future of Work at 1,284 and Social at 1,044.

The nuclear theme itself ranks fifth at 934 postings, reflecting specialist domain hiring distinct from general operational roles. Renewable energy at 871 and cybersecurity at 870 are effectively tied for sixth and seventh. Cybersecurity in a nuclear context is not a general IT theme; it is a critical infrastructure protection requirement. Its presence at that scale signals where the compliance investment is going. Renewable energy alongside it indicates that the operators building nuclear capacity are simultaneously preparing for a portfolio that extends beyond a single generation source.

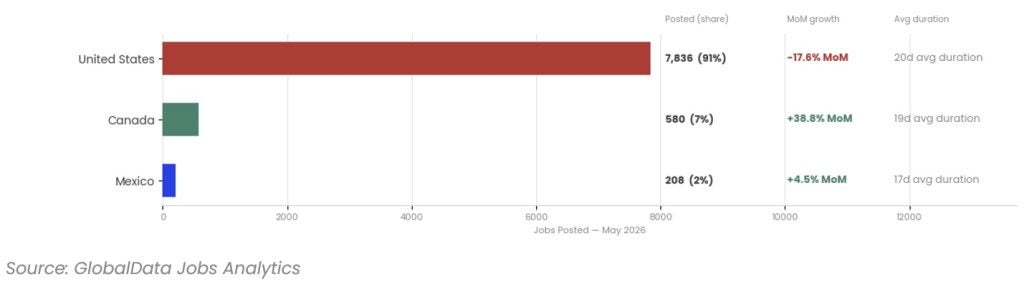

The Canada signal is clean and operator specific

The US accounts for 7,836 of 8,624 posted jobs in May 2026, 91% of the total, and is down 17.6% month-on-month against a 20-day average posting duration. Canada, at 580 postings, is up 38.8% month-on-month with a 19-day average duration. Mexico posts 208 roles, up 4.5%.

The Canada movement is driven by identifiable operators. Hydro-Quebec accounts for 265 postings with a 62.6% month-on-month increase. Ontario Power Generation adds 63. Canadian Nuclear Laboratories contributes 35. These are not diversified industrials with incidental Canadian exposure; they are core nuclear infrastructure operators in a market expanding its nuclear hiring at a rate not visible in the US headline. Posting durations in the 16 to 19-day range confirm conventional recruitment activity, not a data artefact.

What this means for leaders

Across all sectors, detailed hiring and workforce data provides an early, forward‑looking signal of where investment, capacity and risk are shifting. By monitoring changes in roles, skills and locations before they appear in financial results or analyst consensus, leaders and investors can make better decisions on where to back growth, where to scale back, and how to stay ahead of competitors.

GlobalData Jobs Analytics captures point‑in‑time postings directly from company career pages, tagged by company, sector and theme. To see this in practice, request a data sample today by contacting hirendra.vikram@globaldata.com and download the white paper below to start turning complex hiring patterns into clear signals you can use in planning and investment decisions.