Mining M&A activity has carried momentum into 2026, with early-year dealmaking reinforcing trends identified in 2025 around supply-chain security and capital deployment, according to analysis from White & Case LLP, alongside earlier findings from GlobalData.

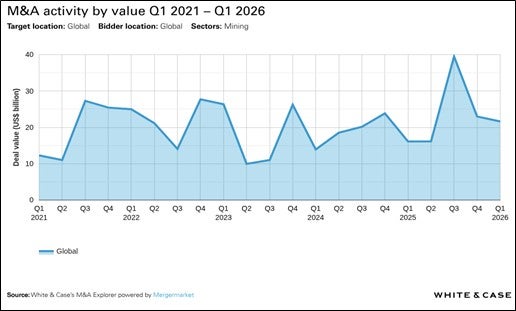

White & Case data shows 121 transactions were recorded in Q1 2026, up from 117 in Q1 2025 and 102 in Q1 2024. Aggregate deal value reached $21.6bn, compared with $16.1bn and $13.9bn respectively, marking year-on-year growth despite the collapse of talks between Glencore and Rio Tinto.

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

The firm said the figures represent the fastest start to a year since 2023 in both volume and value terms.

The Q1 performance follows a strong 2025 for mining M&A. White & Case previously reported total deal value of $93.7bn for the year, while GlobalData, in its February 2026 report Mining M&A Deals 2025 – Top Themes, identified a 35% year-on-year increase in deal value, reflecting sustained capital deployment across the sector .

GlobalData also highlighted supply chain considerations as the primary theme shaping transactions in 2025, with activity concentrated on securing access to critical inputs and downstream processing capacity. This aligns with White & Case’s view that capital is shifting towards assets that support “resilient supply chains for critical minerals”.

Rebecca Campbell, global head of mining and metals at White & Case, said the increase in activity reflects a reallocation of capital towards assets capable of delivering “reliable, long-term supply” in stable jurisdictions.

According to White & Case, transaction decisions are increasingly influenced by jurisdictional certainty, supply continuity and alignment with national priorities, particularly in relation to critical minerals.

GlobalData’s analysis similarly identified supply chain positioning and energy transition-linked assets among the dominant drivers of dealmaking, alongside a rise in large-scale transactions, with mega-deals accounting for a significant share of total value in 2025 .

Survey data from White & Case’s Mining and Metals Survey 2026 indicates that strategic partnerships are expected to be the most common form of transaction this year, cited by 32% of respondents. The firm said this trend is already visible in early 2026 activity, with projects increasingly structured through partnerships involving both private capital and government backing.

Thomas Pate, a partner at White & Case said projects of “long-term importance” are being advanced through such partnerships, alongside more active public-sector participation.

GlobalData’s 2025 review also pointed to geographic concentration in deal value, with North America accounting for the largest share of activity, while other regions recorded uneven growth .

White & Case added that consolidation is expected to continue in certain commodities, with 29% of survey respondents identifying precious metals, particularly gold, as the most likely segment for consolidation over the next 12 months, followed by critical minerals at 27%.