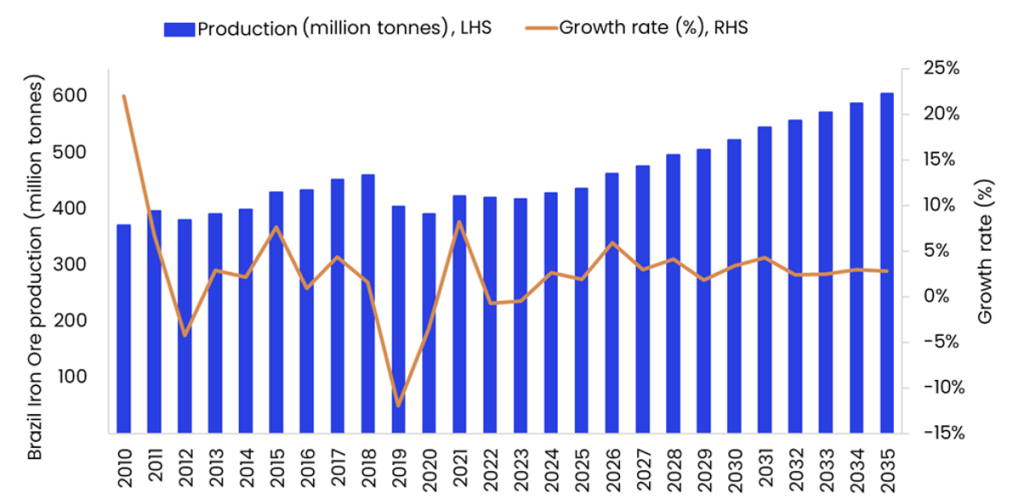

Brazil is the second-largest iron ore producer in the world, accounting for 16.7% of global production in 2024. The country’s iron ore production is expected to have increased by 1.9% in 2025 to 437.2 million tonnes (mt). The growth was primarily supported by the strong production from Vale, the country’s largest iron ore producer. Additionally, the gradual resumption of the pelletizing Plant No. 4 and the ramp-up of the second concentrator at BHP’s Samarco mine in December 2024 further supported the country’s output.

In 2025, Vale’s production reached 336.1mt accounting for 76.9% of the country’s output, making it instrumental in driving the country’s output growth. The Capanema mine within Vale’s Mariana Mining Complex commenced operations in September 2025 and will add 15mtpa to the company’s 2026 production target. In addition, expansion of the Carajas Serra Sul S11D Project, which is scheduled to start in H2 2026, and ramp up of the Vargem Grande 1 (of the Vargem Grande Mining Complex) will further support output growth in 2026.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The upward production trend was partially offset by the lower run-of-mine (ROM) availability at the Serra Norte, elevated maintenance activity at the Itabira, and a strategic pipeline inspection at the Minas-Rio completed in mid-2024. Looking ahead, Brazil’s iron ore production is expected to grow further by 5.9% in 2026 to reach 462.9mt, supported by planned increases at Vale, which is targeting a production range of 335mt– 345mt in 2026. Expansions at other major mines, including Gerdau Mining’s Miguel Burnier and CSN Mineracao’s Casa de Pedra, will further boost the country’s output.

Over the forecast period (2026-2035), Brazil’s iron ore production is expected to grow steadily at a compound annual growth rate of 3.0% reaching 605.7mt by 2035, supported by sustained mine expansions, efficiency improvements across key producing regions and commencement of new mines such as the Block 8, Jambeiro, Morro do pilar, Joao Monlevade, Serro 2030 and Colomi, Amapa and Bamin Restart projects in 2031.

Brazil’s iron ore industry continues to face significant challenges, including environmental concerns, infrastructure bottlenecks, and social conflicts, all of which have contributed to stricter scrutiny and operational disruptions in recent years. Nevertheless, the country remains well-positioned for long-term growth due to its vast mineral reserves and ongoing expansion initiatives by major producers. Supported by resilient global demand, Brazil’s presence as a key iron ore supplier in the global iron ore market is expected to strengthen over the coming years. The Brazilian government is actively updating its mineral policy framework, including a recently launched public consultation to revise the National Mining Plan 2050 for the long-term sustainable development of the sector. Furthermore, in December 2025, the Senate’s Economic Affairs committee approved a proposal to establish a National Policy for Critical and Strategic Minerals. This policy aims to stimulate domestic processing and secure supply chains, a move that could influence investment and production dynamics in the iron ore industry over the outlook period.