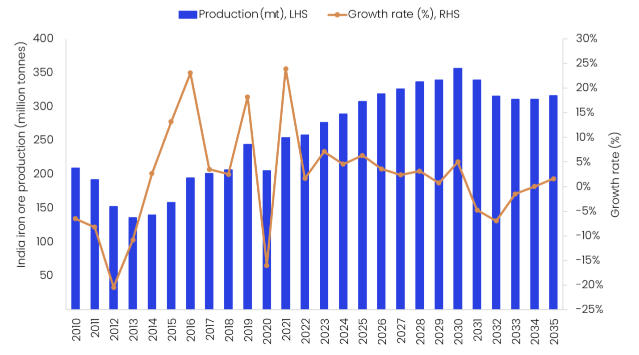

India remains the third-largest iron ore producer in the world and surpassed China for the second consecutive year, accounting for 11.8% of the global total in 2025. The country’s iron ore production is estimated to have increased by 6.3% in 2025 to 307.7 million tonnes (mt), reflecting consistent production and sustained mining expansion from major mines such as the Bailadila iron ore mines (Bacheli and Kirandul Complex), Nuagaon, Noamundi and Katamati mines as companies aim to increase iron ore production.

Looking ahead, India’s iron ore production is anticipated to grow further in 2026 to reach 318.8mt – a 3.6% year-on-year (YoY) increase. This growth will be underpinned by continuous strong production and ongoing capacity expansions from key producing mines such as the Guali Iron ore Mine, Nuagaon, Naomundi and Bailadila Iron ore mines (Bacheli and Kirandul Complex). In India, most of the mines have an annual production below 10mt. Some mines fall within the range of 10mt-30mt, while only a limited number of mines produce more than 30mtpa.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

India produced 266.6mt of iron ore in the first 11 months of 2025, up by 3.9% YoY. The increase can largely be attributable to the efforts of domestic iron ore giants such as National Mineral Development Corporation (NMDC) and Steel Authority of India Ltd (SAIL).

The Indian Ministry of Mines’ amendments to the Mines and Minerals (Development and Regulation (MMDR) Act in recent years have created a more favourable regulatory environment for Indian mining operations, encouraging investment and accelerating production. Leading mining companies like NMDC, SAIL, and Tata Steel are investing in capacity expansion and operational optimisation to capitalise on the growing demand.

The 2025 MMDR Amendment Act further strengthens the mining framework by broadening the scope of the National Mineral Exploration and Development Trust, enabling greater exploration and development financing to improve structured capacity expansion across the sector.

Over the forecast period (2026–2035), India’s iron ore production is anticipated to decline with a negative compound annual growth rate (CAGR) of 0.1%, to 316.1mt by 2035, due to the planned closure of 32 mines, which collectively produced 67.4mt in 2024, but will deliver only 0.3mt in 2035. Amongst the mines planned to close are the Roida II (2026), Mahamaya (2030), Guali Iron Ore Mines (2031), Meghahatuburu (2032), Barsua and Balda Block (2033).