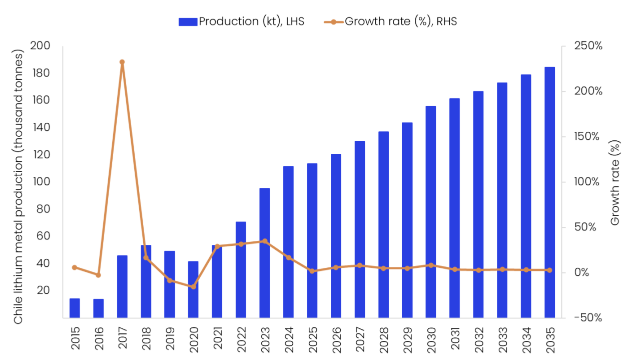

Chile’s lithium production is expected to continue growing in 2026, supported primarily by rising output from the Salar de Atacama, the country’s main lithium-producing hub. Production increased by an estimated 10.1% to 64,100 tonnes (t) in 2025, driven by higher supply from SQM’s Salar de Atacama operations amid ongoing capacity expansion. Output is forecast to rise by a further 4.9% to 67,300t in 2026, indicating that near-term growth remains operationally driven rather than dependent on immediate policy change.

Chile remains the world’s second-largest lithium producer after Australia, with production concentrated in brine-based lithium carbonate operations in the Salar de Atacama in the Antofagasta Region. SQM and Albemarle continue to dominate domestic output, highlighting the highly concentrated nature of the country’s lithium sector. As a result, changes in production at the Salar de Atacama have an outsized influence on Chile’s overall lithium supply outlook.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

While 2026 production growth is expected to be supported by existing operations, the policy backdrop has shifted following the change in government in March 2026. On 11 March 2026, President Jose Antonio Kast assumed office, marking a political transition that could influence the medium- to long-term direction of Chile’s lithium sector. One of the new administration’s early structural decisions was to merge the Ministries of Mining and Economy into a single portfolio, indicating an intention to align mining policy more closely with broader economic and investment objectives.

The new government has signalled a more market-oriented approach to the sector. Kast has expressed the view that Chile’s existing lithium framework concentrates resource access among a limited number of operators, constraining competition and discouraging broader private investment. His policy stance favours lower regulatory and tax burdens, improved legal certainty, and a more investment-friendly framework aimed at attracting a wider pool of domestic and international capital into the mining sector.

However, despite the political change, the near-term operating framework for lithium remains largely unchanged. As of mid-March 2026, no material legal reforms had been introduced, and lithium remains a non-concessionable resource under Decree Law No. 2886. Any significant change to the legal structure would require amendments to the National Mining Code through Congress and the Senate, where the government does not have unrestricted legislative room. This suggests that the current project pipeline is likely to continue under the existing model in the near term.

Chile’s present lithium framework was largely shaped under the Boric administration, which introduced the National Lithium Strategy in April 2023. The strategy established a state-led model under Codelco’s oversight, while allowing private participation through public-private partnerships in which the state would retain majority ownership. This policy direction led to the creation of Nova Andino Litio in December 2025, a joint venture between Codelco and SQM to manage and develop lithium extraction in the Salar de Atacama.

Regulatory momentum also strengthened in 2025 through the rollout of a more streamlined application process for special lithium operating contracts, or CEOLs, across multiple salt flats, including Agua Amarga, Ascotan, and Coipasa. In September 2025, Enami signed the first CEOL, marking an important milestone for the development of the Salares Altoandinos project in the Atacama Region. Although the new administration may seek to reshape the sector over time, indications so far suggest that the Nova Andino Litio structure is unlikely to be revisited immediately, while the CEOL-based model remains the practical route for advancing new lithium projects in the near term.

The new administration has also signalled stronger external alignment with the US on critical minerals policy. On his inaugural day, Kast signed broad critical minerals agreements with the US, reflecting a more outward-looking strategy that could strengthen Chile’s position in Western supply chains for battery materials. Even so, these agreements are more likely to influence long-term investment direction and strategic partnerships than immediate 2026 production outcomes.

Over the forecast period, Chile’s lithium production is projected to grow at a modest compound annual growth rate (CAGR) of 2.9% to 87,200t by 2035. This growth is expected to be supported by the planned commissioning of Enami’s Salares Altoandinos Lithium Project and Cleantech Lithium’s Laguna Verde in 2027, followed by Codelco’s Maricunga project in 2030. While these developments support a positive long-term outlook, execution will depend on regulatory clarity, project financing, and the extent to which the new government translates its investment-friendly rhetoric into workable sector reform.