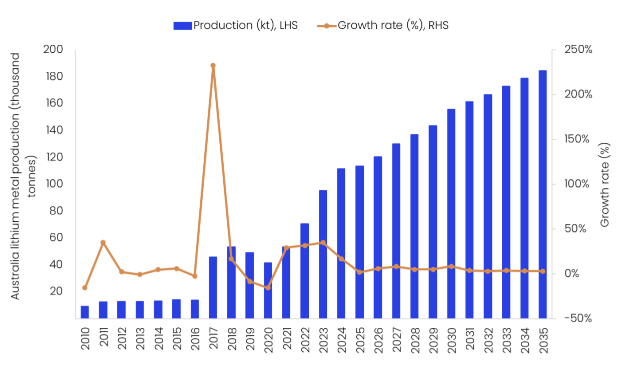

Australia remains the world’s largest lithium producer, accounting for 33.5% of global lithium output in 2025. The country’s lithium mine production is estimated to have increased to 113,500 tonnes (t) in 2025, a 1.8% marginal growth over 2024. This limited growth was primarily supported by the ramp-up of Liontown Resources’ Kathleen Valley project and SQM’s Mt Holland lithium project, both of which commenced operations in mid-2024, alongside ongoing expansions at the Pilgangoora and Greenbushes lithium operations.

However, persistently weak spodumene prices and cost-cutting measures have prompted several producers to scale back operations. Key examples of this market-driven consolidation include PLS Group Limited (formerly Pilbara Minerals) placing its Ngungaju plant under care and maintenance in December 2024, Mineral Resources (MRL) suspending operations at its Bald Hill project in November 2024 (which remains suspended as of January 2026), and Rio Tinto Lithium halting operations at Mount Cattlin in March 2025. Collectively, these shutdowns highlight a strategic industry shift toward capital preservation and operational rationalisation in response to the current pricing downturn.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Looking ahead, Australia’s lithium output is expected to rebound in 2026, with production projected to grow by 6% to reach 120,300t. This growth will be driven primarily by operational enhancements and capacity expansions at key mining sites. A major contributor will be the Kathleen Valley project, which completed its phased transition from open-pit mining to a fully underground operation on 21 December 2025, and is now ramping up production as planned. This transition is aimed at targeting higher-grade ore, improving operating margins, and enhancing long-term operational efficiency and sustainability.

Further upside to output growth is expected from continued expansion activities at the established Greenbushes lithium operations and the Pilgangoora project, both of which are set to contribute materially to overall supply growth through 2026, reinforcing Australia’s position in the global lithium market.

From a policy perspective, the Australian Government is actively attracting investments in the critical minerals industry through the Critical Minerals Strategy 2023–2030 and the “Future Made in Australia” plan. These include significant funding and tax incentives (a 10% production tax incentive for processing and refining costs) to encourage private investment in the critical minerals sector.

In February 2026, the Australian Government released its Critical Minerals Prospectus, profiling 78 investment-ready projects from 60 companies, including one lithium project. The prospectus also listed 29 midstream processing opportunities, four of which were lithium-related. Core Lithium’s Finniss Lithium Operation was shortlisted in the upstream category while Albemarle’s Kemerton lithium hydroxide processing plant, Tianqi Lithium Energy Australia’s Kwinana lithium hydroxide refinery, Livium’s Livium project, and Li-S Energy’s lithium metal foil line were shortlisted under midstream processing.

Over the forecast period, Australia’s lithium mine production is forecast to grow at a compound annual growth rate (CAGR) of 4.9% between 2026 and 2035, reaching 184,500t by 2035. Key projects scheduled to commence operations during the forecast period include the Mount Finniss Restart Project (2028), Pilgangoora Expansion (P2000), Tabba Tabba, Lithium and Manna lithium projects in 2030, which are expected to underpin sustained production growth beyond the current market downturn.