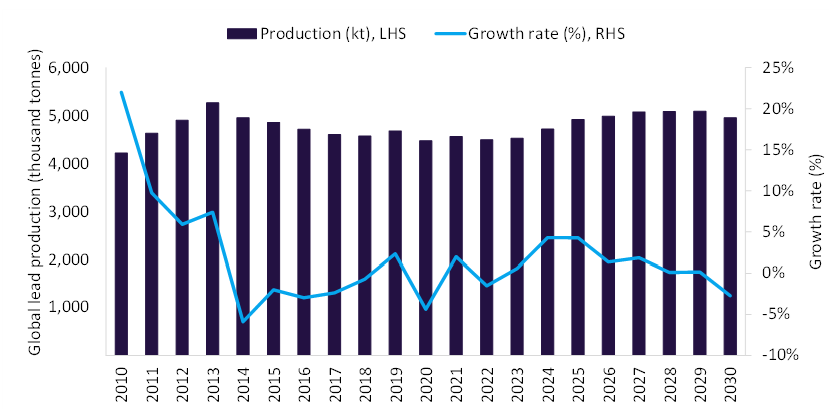

Global lead production is expected to grow by 4.3% to more than 4.7 million tonnes in 2024.

The increase will predominantly be fuelled by rising output from key producers such as Australia, the US, and Russia.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Australia is expected to deliver the highest lead production growth in 2024, driven by its Abra and Federation projects.

Russia’s Ozernoe and Prognoz and the US’ Hermosa project will also contribute to the global increase.

Australia accounted for 9.2% (414.4 kilotonnes) of the total global lead supply in 2023.

Despite a 5.3% dip in output in 2023 due to adverse weather conditions and planned ore grade reductions, its output is expected to recover in 2024, with forecast production of 484.6 kilotonnes.

Reports

Lead Mining Market Analysis by Reserves, Production, Assets, Demand Drivers and Forecast to 2030

This will be supported by the ramp-up of the Abra Base Metals mine and the commencement of the Federation Underground project, which is one of Australia’s premier high-grade base metal ventures.

Wholly owned by Aurelia Metals, the project is expected to have an annual saleable lead production capacity of 29 kilotonnes. It is currently in the construction phase and is on track to commence operations in the third quarter of 2024.

Meanwhile, global lead production in 2024 will be further bolstered by increasing output from Brazil’s Aripuana Zinc project, alongside the initiation of new ventures such as Russia’s Ozernoe and Prognoz, and the Hermosa project in the US.

In contrast, China, the world’s largest lead miner, is anticipated to show relatively stagnant output in 2024, with a modest 0.9% year-on-year increase.

This is attributed to sustained production levels in existing mines and a lack of new capacity additions.

The Republic of Ireland’s output will face challenges as Boliden’s Tara mine has been in care and maintenance since July 2023, due to adverse cashflows stemming from a decline in commodity prices.

Looking ahead, global lead production is expected to show marginal growth over the decade, with a compound annual growth rate (CAGR) of 0.8% from 2024 to 2030, as output reaches 4,954.4 kilotonnes in 2030.