Australia’s coal mining industry remains a critical pillar of the national economy, with thermal coal accounting for more than 60% of total output and metallurgical coal comprising the remainder.

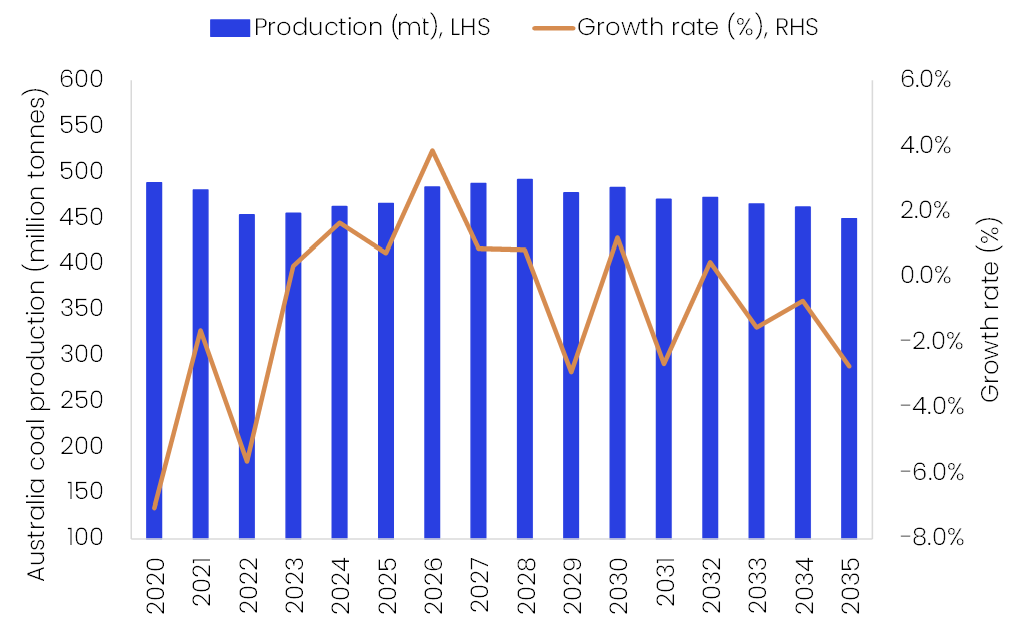

Total coal production is estimated to have remained broadly flat in 2025 at 65.3 million tonnes (mt), reflecting only marginal growth over 2024. This stability was underpinned by the continued ramp-up of the Olive Downs Complex, which commenced operations in June 2023, alongside planned production increases at the Saraji, Maules Creek, and Burton mines, and improved stripping ratios and operational efficiency at the Hunter Valley and Dawson mines.

These gains were largely offset by lower output from the Ulan coal underground mine due to operational constraints and a temporary suspension of operations at the Moranbah North mine, following a fire in March 2025.

In 2026, coal production is forecast to increase by 3.9% to 483.2mt, driven primarily by a series of operational developments. Key contributors include the continued ramp-up of the Maxwell underground project, planned increasing capacity at the Byerwen and the Narrabri underground mines, and higher output from the New Acland mine following the receipt of mine life extensions.

Production is also expected to recover at the Ulan mine as operations normalise following the resolution of prior-year constraints. These gains will be partially offset by lower contributions from mature mines such as the Wilpinjong and Springvale, and the closure of Glencore’s Integra mine in 2025.

Over the forecast period (2026-2035), Australia’s coal production is projected to enter a structural decline. Output is expected to contract at a negative CAGR of 0.8%, falling to 448.7mt by 2035. This subdued trajectory reflects a combination of long-term supply-side and demand-side pressures, including the scheduled closure of several key mines such as the Griffin coal mine (2026), Clermont coal mine, Springvale mine and Cook Colliery (2028), and the Chain Valley Colliery and Oaky Creek mine (2029), which collectively produced 132.1mt of coal in 2024.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The production outlook will be further constrained by weakening global demand for thermal coal, as renewable energy and natural gas increasingly displace coal-fired power generation in major consuming markets, including the US and China. This demand erosion is expected to accelerate the decline in output triggered by mine closures and limit incentives for large-scale new capacity additions.

From a regulatory perspective, Australia’s mining sector is undergoing a material transformation amid rising environmental and sustainability pressures and a strategic shift toward critical minerals. The introduction of stricter environmental regulations, including the Environment Protection Reform Act 2025, is increasing approval scrutiny, compliance costs, and project development timelines, particularly for coal mining projects. While clearer regulatory frameworks are intended to enhance transparency and long-term investment certainty, they are also expected to act as a near-term headwind to coal sector expansion.