The Democratic Republic of the Congo (DRC) continues to dominate global cobalt supply, accounting for around 72% of total production in 2025. This leading position is underpinned by the country’s vast cobalt resources and long-standing strategic partnerships with Chinese mining companies, which have enabled large-scale mine development and sustained output growth.

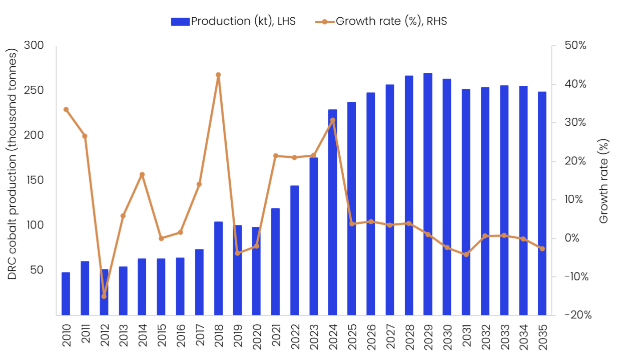

The country’s cobalt mine output is estimated to have increased by 3.7% to reach 237,300 tonnes (t) in 2025. Supply growth was driven primarily by higher grades and expanded volumes from Glencore’s Mutanda mine, alongside the commencement of underground operations at the Musonoi project in September 2025. The Musonoi project, jointly owned by Jinchuan Group (75%) and Gécamines (25%), has a production capacity of around 7,400t of cobalt and an estimated mine life of up to 14 years, strengthening the country’s medium-term supply outlook.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The production trajectory is further supported by consistently strong output from China Molybdenum’s (CMOC) major operating assets in the DRC, particularly the Kisanfu (KFM) and Tenke Fungurume Mining (TFM) operations, which remain key contributors to national cobalt production. However, some of this growth has been partially offset by the suspension of operations at MMG’s Kinsevere mine in December 2024, reflecting challenging market conditions marked by cobalt oversupply and declining prices.

Looking ahead, cobalt production in the DRC is projected to continue rising in 2026, with a 4.4% annual growth rate, supported by higher-grade feed from the Mutanda and the ramp-up of the Musonoi underground project. Despite short-term market headwinds, these operational developments are expected to sustain positive production momentum.

China’s influence in the DRC’s mining sector has been reinforced through the long-standing “minerals-for-infrastructure” (Sicomines) agreement, originally signed in 2008. Under this framework, Chinese companies gained access to large copper and cobalt resources in exchange for infrastructure development financed by mining revenues. While the agreement has delivered capital and technical expertise, it has also raised concerns around economic sovereignty, benefit sharing, and policy influence.

In response to prolonged domestic criticism, the Sicomines agreement was revised between January and March 2024. The revised terms increased infrastructure funding commitments to $7bn, up from $3bn, extending to 2040. Chinese operators continue to benefit from tax, duty, and royalty exemptions until 2040; however, the revised deal raises annual royalty payments to the DRC Government to 1.2% and introduces a profit-sharing clause that allocates an additional 30% of profits to infrastructure funding if copper prices exceed $12,000 per tonne, improving alignment with national development objectives.

Currently, many of the DRC’s largest operating cobalt mines remain under Chinese ownership. CMOC, in particular, has emerged as a dominant player through its ownership of key assets such as TFM, KFM, and the Kamoto Copper Company (KCC). Nonetheless, the DRC Government is increasingly seeking to attract non-Chinese investment to reduce concentration risks and diversify control within its mining sector.

To this end, the DRC has begun strengthening partnerships with alternative international investors. In December 2025, the US International Development Finance Corporation (DFC) announced plans to provide $1bn to support a new copper and cobalt venture involving Gecamines and Mercuria Energy Trading, alongside financing a regional rail corridor linking the DRC to Angola’s coast. In parallel, the US and DRC are exploring a “minerals-for-security” arrangement that would grant the US secure access to critical minerals such as cobalt, lithium, and uranium in exchange for military and investment support aimed at improving regional stability.

Beyond the US, the DRC is actively engaging with investors from Saudi Arabia, the European Union, and India as part of a broader strategy to diversify funding sources, reduce reliance on China, and strengthen the resilience of its mining sector over the long term. Over the forecast period (2026-35), DRC’s cobalt production is anticipated to grow with a compound annual growth rate (CAGR) of 0.03%, to 248,300t by 2035, based on known projects. This slow growth is attributable to the planned closure of three mines such as the Kalongwe Project (2029), Deziwa Project (2030) and Etoile Mine (2032), which collectively produced 20,430t in 2025.