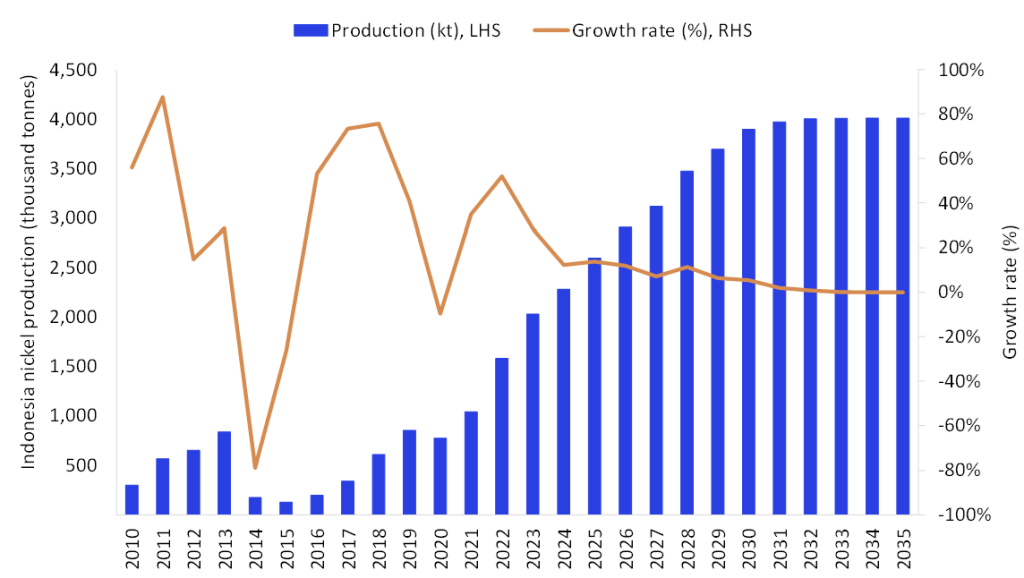

Indonesia is the world’s largest nickel producer, accounting for around 65% of global output. In 2025, production is estimated to have increased by 13.9% to 2.6 million tonnes (mt), driven by higher mine output from the Weda Bay, Gag Island, Huafei, Pakal Island, Pomalaa, PT Halmahera Persada Lygend, and Tapunopaka mines. Collectively, these operations reinforce Indonesia’s role as the primary source of incremental global nickel supply.

Weda Bay is expected to record higher nickel production in 2025–2026, supported by increased permitted mining volumes and stronger domestic processing demand. A revised RKAB approved in July 2025 raised permitted production for that year to 42 million wet metric tonnes (mwmt) per annum from 32mwmt, including an additional 10mwmt of limonite ore, lifting supply capacity as new NPI and HPAL plants are commissioned. Over the longer term, following AMDAL approval and a feasibility study in 2024, Eramet plans a ramp-up towards around 60mwmt per annum, supporting continued production growth beyond 2026. Additional support is expected to have come from the ongoing ramp-up of Zhejiang Huayou’s Huafei cobalt-nickel project, which began production in Q1 2024.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

China-led foreign direct investment has been the main catalyst behind Indonesia’s nickel boom, enabling a rapid build-out of smelters and industrial parks and accelerating the shift from exporting raw ore to exporting higher-value refined and battery-linked products. This transformation was reinforced by Indonesia’s downstream agenda—anchored by the 2009 domestic processing requirement and tightened by the 2020 nickel ore export ban—which redirected capital into domestic processing and lifted output of products such as ferronickel, nickel matte and, increasingly, battery intermediates.

RKAB (Rencana Kerja dan Anggaran Biaya) is Indonesia’s work plan and budget approval for mining, used by regulators to control permitted operating and production plans. While approvals had previously been aligned to an integrated three-year framework, the government is reintroducing annual RKAB approvals from 2026, which effectively increases the frequency of oversight. This shift gives policymakers more flexibility to tighten approvals when needed, especially as rapid capacity additions have contributed to oversupply and weaker prices.

Despite these policy signals, nickel output is still set to rise by 11.9% in 2026 to 2.9mt, as the commissioning pipeline remains strong and much of the capacity expansion is already “built-in” from prior investment decisions, particularly from Chinese-backed firms. A major contributor is the continued ramp-up of high-pressure acid leaching (HPAL) capacity for battery materials, where projects nearing mechanical completion tend to push volumes higher once they enter start-up and commissioning.

PT Vale Indonesia captures the tension between intended restraint and industrial momentum. The company’s RKAB approval came in at roughly 30% of what it requested, warning that this may not fully meet ore requirements for its incoming plants. At the same time, Vale and partners are advancing HPAL developments tied to 2026 timelines—Pomalaa is targeting mechanical completion around August 2026 and is designed for about 120 kilotonnes per annum of MHP, requiring around 21mtpa of limonite feed, while the Morowali/Bahodopi HPAL is designed for about 66 kilotonnes of MHP, requiring around 10.4mtpa of limonite.

With multibillion-dollar investments committed, these projects create strong upward momentum for production even if the quota policy becomes tighter. The result is a clear push–pull dynamic for 2026. Policy may aim to cap supply growth, but commissioning schedules and entrenched expansion plans keep the production trajectory pointing upward.

Over the forecast period, the country’s production is expected to grow at a compound annual growth rate (CAGR) of 3.6% to reach 4.0mt in 2035. This will be supported by the consistent output from the existing mines along with upcoming projects.

Key upcoming projects include the Morowali and Pomalaa projects in 2026 and the Sorowako limonite project in 2027. Overall, the country’s objective to expand its nickel smelting capacity will further encourage domestic production.