Graphite is a crucial element in many industrial processes, as well as being a critical component of lithium-ion batteries – and by extension the expansion of electric vehicles (EVs).

With it comprising the battery’s anode, or negative terminal, graphite will continue to play a central role in the energy transition.

However, as with so much of the world’s critical minerals, a large proportion of graphite reserves sit under Chinese control. Research from GlobalData, Mining Technology’s parent company, indicates that China held 81 million tonnes (mt) of natural graphite reserves in 2025, or almost 28% of the world total.

China was also the leading graphite producer in 2024, accounting for 82% of the global total with an output of 1,270 thousand tonnes (kt).

This represents a series of challenges for the global supply chain, particularly when exports controls, tariff threats and simmering geopolitical tensions come into play.

Concerns have been growing regarding China’s dominance of graphite production and it feeding the global supply chain. As such, the US and Australia (among many nations) are attempting to develop domestic graphite resources.

For example, the US Department of Commerce recently amended its initial May 2025 finding (a preliminary countervailing duty determination) for active anode material from China, citing “significant ministerial errors in the original calculations”. The ruling aims to reduce US dependency on Chinese graphite inputs and support domestic battery supply chain resilience.

The EU classifies graphite as a critical raw material, prompting efforts to secure supplies and develop European sources, and subsequently leading to more interest in potential graphite deposits in Sweden and Finland.

The European Commission has adopted a list of 60 strategic projects to enhance domestic raw material capacities under the Critical Raw Material Act (CRMA). It includes 15 projects focused on graphite (11 inside the EU and 4 internationally).

China’s supply chain threat

“China’s graphite monopoly poses a threat to global supply chains and countries dependent on graphite imports, as the country dominates procurement (especially in Africa and South America) and processing,” says Martina Raveni, analyst at GlobalData.

“The monopolisation of such essential resources has caused global concern as the availability and market price are contingent on Chinese export policies,” she adds.

In July 2023, in response to the US restricting exports of key semiconductor equipment and components to China, Beijing started requiring additional export permits for several minerals, including graphite.

Then, in late 2024, “the country announced further export controls for graphite, specifically to the US”, adds Raveni, predicting that “China will likely continue to restrict graphite exports, using its position as the primary producer and refiner”.

China occupies a dominant position in global EV battery production, accounting for more than 75% of sales, according to GlobalData, adding that Chinese auto makers have a cost advantage driven by manufacturing expertise, supply chain integration and intense domestic competition.

In December 2024, China imposed export restrictions (essentially government permits) on key anode materials, mostly hitting exports of high purity (at around 99%) synthetic graphite and naturally occurring flake graphite.

The move by Beijing – which still holds a dominant (if weakening) position in the global graphite industry, and accounts for more than 60% of flake graphite and nearly 80% of synthetic graphite production globally – was likely a way to safeguard domestic interests.

Belinda Labatte, executive chair of the board of directors at Lomiko, a Canadian critical minerals developer, says: “As has been widely reported, China has carefully constructed a chokehold strategy of economic hegemony so, yes, having one country with all the elements of a defence and new tech supply chain is a problem.”

She notes that China is now increasing its annual spend on critical minerals to $13bn (93.28bn yuan) per year, “as the US and other countries assertively counter China’s supply chain dominance with increased spending on public/private investments in critical minerals”.

“With a new government leader in place, Canada has made dramatic and significant improvements to build a new industrial plan for Canada that will support and promote critical minerals projects,” adds Labatte.

She points to “Argentina, Brazil and Mexico, [which] lean on Chinese funds set up for a purpose. Economic warfare through supply chain dominance is the new generational battle we are in.”

"We do not need regulations to loosen, but we do need to transform how we work to transform ourselves from a capital markets-based approach to funding to a public/private partnership approach," adds Labatte.

Corina Hebestreit, secretary general at the European Advanced Carbon and Graphite Materials Association, agrees that it is also not “a question of loosening legislation, but more a question of speedy and unconfrontational implementation of existing legislation”.

Hebestreit says that whether China’s global graphite dominance is a problem is a matter of perspective. “From a Chinese perspective, certainly not; from a US or European and a NATO perspective, certainly yes. This is why all these entities have decided on policies to increase [their] own supply, or at the very least diversify sourcing.”

"Actually, graphite as such is not a scarce resource: it is the accessibility and the availability of investments that is restricting the access to natural graphite," adds Hebestreit.

China’s graphite resources and production

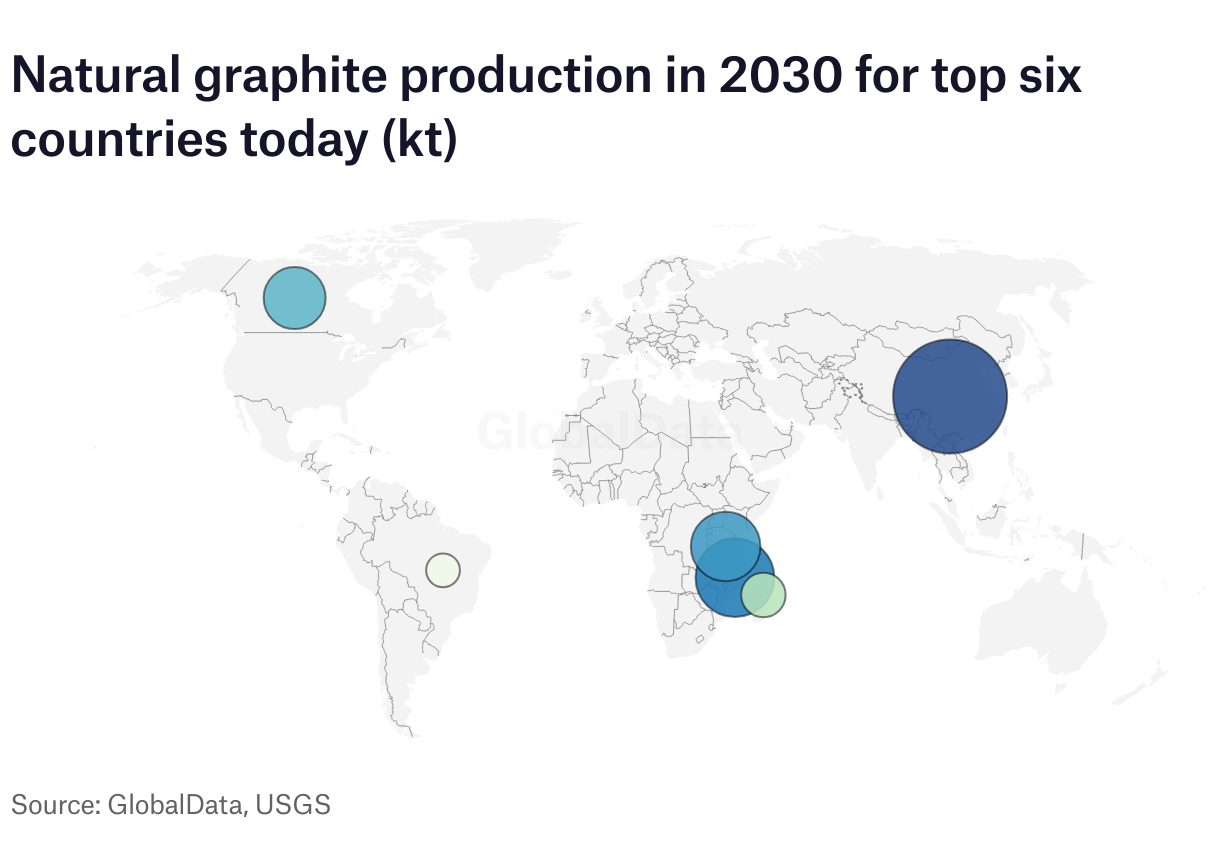

According to GlobalData’s Global Graphite Mining to 2030 (2025 Update) report, global natural graphite reserves stood at 290mt as of January 2025. China hosts 28% of global graphite reserves.

Global natural graphite production is expected to grow at a compound annual growth rate of 15.6% to more than 3.78mt by 2030, mainly due to scheduled commencement of new projects in Mozambique, Tanzania, China, Canada and Australia. After an estimated 1.3% growth in 2024, global natural graphite production is expected to increase by a substantial 18.1% to reach 1.83mt in 2025, adds the report.

“There have already been demonstrations of interest in expanding natural graphite production by developing new mines and increasing the output of existing ones internationally,” says Raveni.

Madagascar, the second-largest producer of natural graphite after China, is likely to see graphite production growth, backed by the Molo graphite project, says Raveni, coupled with the ramp-up of the Sahamamy and the Vatomina projects.

According to the US Geological Survey, cited by the GlobalData report, around 15% of the graphite produced in China was amorphous graphite, with the remaining 85% being flake graphite, commonly used in EV batteries.

Going green with graphite

“Graphite is important to many green technologies, including batteries for EVs and hydrogen fuel cells,” says Raveni. “Demand for it will likely increase substantially in the coming years as pressure to reach net zero intensifies.”

In fact, she adds that the EU is particularly keen to position itself as a pioneer of green hydrogen technology, and the scale-up of hydrogen power would put pressure on graphite supplies.

“Synthetic graphite – purer and better suited to long-life applications than natural graphite – is widely used by EV battery makers,” says Raveni, but it “costs more than double the price of natural graphite, and its production is very energy-intensive, with a large carbon footprint. Therefore, the market value of graphite is strongly tied to power rates and susceptible to price surges.

“Legislation restricting carbon emissions within the US and Europe makes setting up a strong domestic synthetic graphite industry difficult,” adds Raveni. “Despite being of lesser quality, natural graphite may become more popular in response to Chinese dominance and net-zero initiatives.”

Aidan Knight, associate analyst, GlobalData Strategic Intelligence, points to several ways mining companies can mitigate the environmental impact of the graphite industry.

“They can implement cleaner mining technologies such as dry processing, dust suppression systems (water misting, fog cannons, or chemical suppressants), and enclosed processing plants to reduce fugitive dust and water usage,” he says.

Water usage and management are other areas that can be improved, he adds. Closed-loop water systems recycle process water and minimise discharge, lined tailings storage facilities can prevent groundwater contamination, and water treatment systems can remove heavy metals and fine particulates from water, reducing environmental contamination.

The outlook for graphite supply

Despite China’s current dominance in graphite supply and production, political moves are under way to break Beijing’s hold and establish different production channels.

There is a significant opportunity here for Western nations to capitalise on the ever-growing demand for graphite to develop and shore up non-Chinese supply chains.

Whether the same can be said for other critical minerals China has under its control remains to be seen.